Lower fees without and no fees for currency exchange

Direct access: #Strategies #Fund list

Advantages

Your advantages with finpension pension funds

Within the framework of vested benefits, you can decide for yourself how your assets from second pillar are invested. The securities solution from finpension offers the following advantages:

Cheaper

Better

Better performance thanks to exemption from foreign taxes on dividends

Higher

Higher interest rates on bond and money market funds than on a account

More effective

More effective thanks to advance payment of withholding tax reclaim

Investment strategies

Invest your vested benefits in values that are important to you

We have put together six investment strategies for you with varying degrees of equity exposure. The strategies are available in three different versions, Global, Switzerland and Sustainable.

Each strategy can be adapted individually. You decide. But don’t worry, we will help you.

App Features

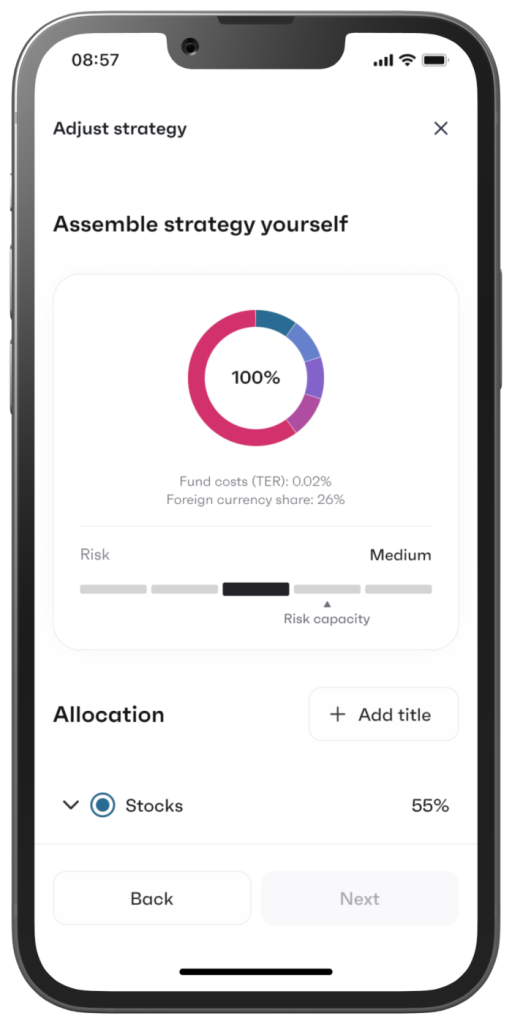

Custom Strategies

For those who want more flexibility, finpension offers the ideal solution: custom investment strategies.

With just a few clicks, adjust the weights of different investment instruments or replace them. Thanks to filter and search options, you can quickly find the right instrument.

All relevant information is always available, as fund factsheets are also linked to the investment instruments.

Fund house

Institutional pension funds in which large pension funds also invest

Your strategy is implemented with the zero-free funds of Credit Suisse, Swisscanto or UBS.

The fund houses are all on a par. None is superior to the other. Choose one of the fund houses according to your preference, or combine the funds as you wish with an individual strategy.

Swisscanto

Your strategy is implemented with Swisscanto’s index funds. Swisscanto is owned by Zürcher Kantonalbank.

UBS

Your strategy is implemented with the UBS index funds.

ex Credit Suisse

Your strategy is implemented with UBS index funds (former Credit Suisse Index Funds).

Fees

A flat-rate fee – fund costs included

The investment strategies offered are implemented with zero-free funds. This means that there are no additional costs for the TER. They are included in the flat-rate administration fee.

No transaction or custody fees are charged.

0.49%

Fees

Transparent fees cannot be taken for granted

But the low flat-rate fee is not enough. Compared to other providers, you also save where you might not even realise it. Here are a few examples:

No margin when changing into other currencies

No issuing commission

Withholding tax exemption

Added value

High added value for your occupational benefit scheme

One percent more or less. Who cares about that? But watch out: Over time, a supposedly small difference can make a lot of money. Take a look for yourself:

Basis for calculation:

Investment period of 25 years, average annual return of 3.25%, including an additional return of 0.75% compared to competitors due to lower investment costs and withholding tax optimisation.

Process

Investing vested benefits: For all those who strive for more

Would you like to get more out of your vested benefits? With shares, you have the chance of a significantly higher long-term return than with a vested benefits account. You also benefit from dividends that do not have to be taxed as income.

Open a vested benefits deposit account

Register in the finpension app by opening a portfolio.

Step

1

Transferring vested benefits

Have an existing vested benefits account transferred to finpension.

Step

2

Automated investment

Your deposit is always invested in your investment strategy on the second bank working day of the week.

Step

3

Get more from your pension

If you invest your vested benefits for the long term, you have a good chance of achieving significantly higher pension fund assets than with a vested benefits account.

Target

FAQ

Questions & answers about the vested benefits custody account from finpension

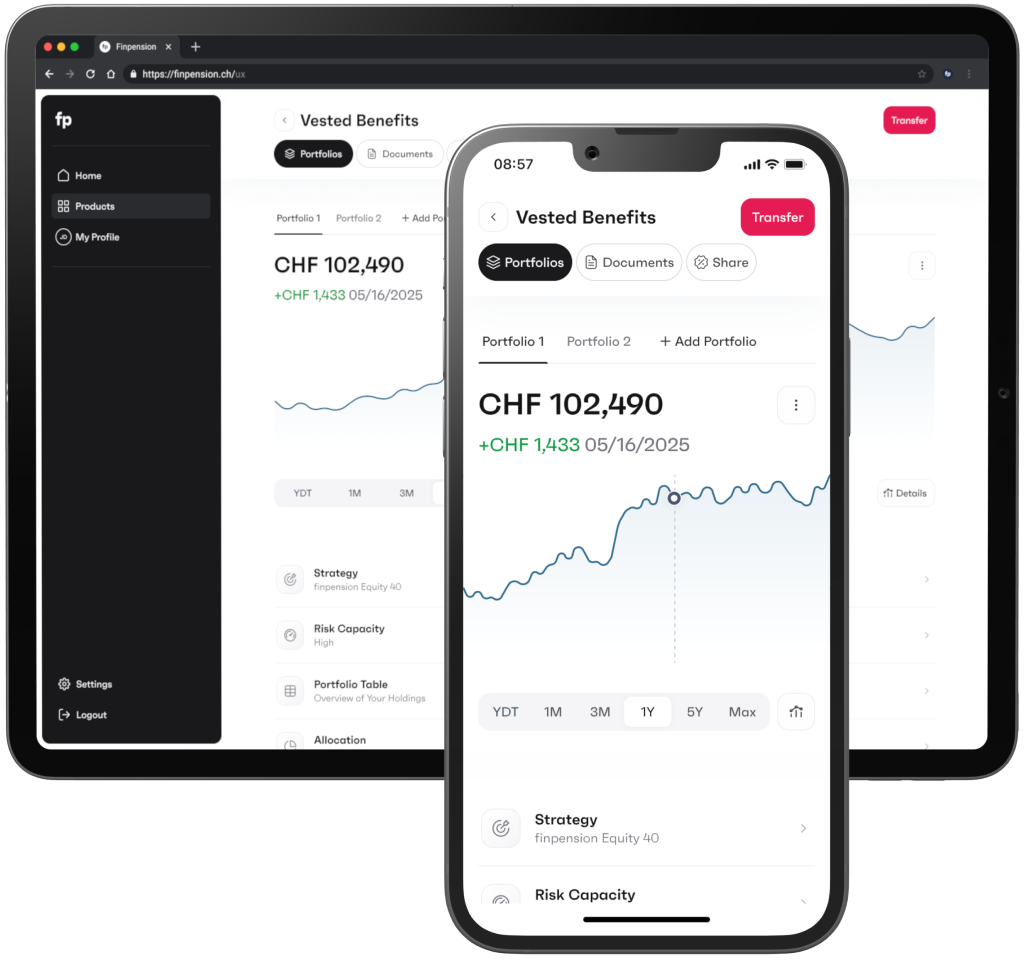

What is a vested benefits custody account?

The vested benefits portfolio is designed to invest the funds from your vested benefits account in securities. Do you have a long investment horizon? In that case, it may be worthwhile to invest your vested benefits in securities rather than keeping them in an account.

How many vested benefits custody accounts can I open?

You can open up to five portfolios with different strategies in “Vested benefits” and “Vested benefits 2”.

Looking to split your pension fund assets? Open two vested benefits portfolios with finpension—one with “Vested benefits” and one with “Vested benefits 2”. You’ll find instructions on how to do this on the page for the Vested Benefits 2.

When is the deposit invested in the vested benefits custody account?

Purchases and sales of fund units always take place on the second bank working day of the week (please note: the settlement of trades is delayed by two to three bank working days).

Before we trade, we check whether other clients have orders to the contrary. Ultimately, we only trade what is necessary on balance. This internal netting is fully automated.

Thanks to netting, we can often settle purchases and sales at better prices than other providers can.

Can I change my investment strategy at any time?

You can change the strategy at any time free of charge. Choose a different standard strategy or customise your strategy. The strategy is implemented on the second banking day of the week.

Is there an automatic rebalancing?

If a fund’s allocation deviates from the target allocation by more than one percentage point, your entire portfolio will be rebalanced. Investments will be sold and purchased to restore the target allocations of the individual index funds.

Rebalancing is carried out weekly on the second banking day of the week. No transaction fees apply. Rebalancing can be deactivated if desired.

Do I have to pay tax on a vested benefits portfolio?

You do not have to pay tax on a vested benefits account. Your pension assets are only taxed when withdrawn, through what is known as the capital withdrawal tax. For this reason, it can be beneficial to keep your vested benefits in the pension system for as long as possible. However, be sure to also consider the advantages of a staggered withdrawal.

Can you withdraw money from a vested benefits portfolio?

No, you generally cannot withdraw money from a vested benefits portfolio. Funds can only be accessed upon retirement or in a few exceptional cases, such as early withdrawal for home ownership, emigration, or starting self-employment.

Web application and mobile app

Register now & try it out without obligation

You can register directly via our web app or by downloading the free finpension app to your smartphone. No minimum fee and no obligation to make a deposit.

- Without obligation and without a minimum contract duration

- Up to 5 independent portfolios

- Free choice between account or securities

- 25 CHF fee credit per referral

Have your health insurance card ready – it contains the AHV number you will need for registration.

Vested benefits