Those who contribute to pillar 3a have two options: leave the money in an account or invest it. This article explains the differences between the two options. And you will learn when it is worth investing in pillar 3a – and what you need to watch out for.

Table of content

Invest in pillar 3a: What is the difference to an account?

When you pay into pillar 3a, you have two options: You can put the money into a 3a account or invest it in securities.

Regardless of whether you choose an account or an investment, the basic rules of pillar 3a remain the same. In both cases, you benefit from tax savings, the money is generally tied up until retirement age and the maximum amount is the same. However, how your pension assets develop differs significantly.

A 3a account works in a similar way to a savings account. The balance earns interest and the interest is credited to the account. Important to know: The interest rate is not guaranteed when you take out the account – banks can adjust it at any time. However, banks generally pay better interest on 3a funds than on other savings accounts.

However, you can also invest your pillar 3a in pension funds or ETFs. In this case, you will not receive a fixed interest rate. How your assets develop depends on the performance of the selected fund. In contrast to the 3a account, the value of the investments fluctuates.

Is it worth investing pillar 3a?

Interest rates on 3a accounts are low, often below 1 %. If your assets are left there, they will lose value over time. The reason: inflation is usually higher than the interest. Your money grows – but too slowly to be able to afford as much. You lose purchasing power.

A 3a investment opens up opportunities for returns that an account cannot offer. You do not receive a fixed interest rate, but participate in the performance of the markets. However, this entails fluctuations that must be endured.

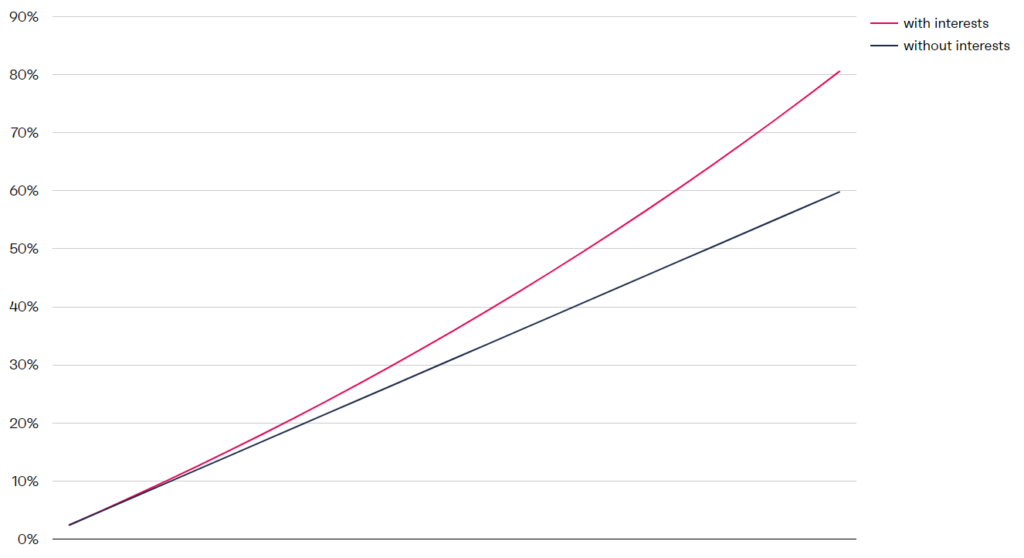

Time and interest – the underestimated duo

The so-called compound interest effect is particularly powerful. The earlier you invest, the longer your capital can grow – and the more you benefit from the returns on your income. The effect is considerable. Let’s assume you achieve an annual return of 2.39 % over 25 years. Then the additional return due to the compound interest effect is a good 20 %.

How does pillar 3a investing work?

When you invest your pillar 3a, this is usually done via pension funds or ETFs. These invest the money from you and other investors in various asset classes – such as shares, bonds, property or commodities.

You do not have complete freedom of choice. This is because pension assets are subject to legal requirements. They must be invested broadly – this is known as diversification. The advantage? Diversification protects your assets if individual investments underperform.

Difference between pension funds and ETFs

Pension funds are specially designed for pillar 3a. They invest exclusively pension assets and are therefore exempt from withholding tax. This means that interest and dividends are fully reinvested.

If you invest your pillar 3a assets with an ETF, this advantage does not apply.

What do I need to consider when investing my pillar 3a?

If you want to invest your pillar 3a, you should keep a few points in mind – from the costs and strategy to your own risk capacity.

Compare providers and fees

Not all offers are the same. Pay attention to the cost structure and what is included in the fees – for example, the costs for funds (TER) or foreign currency exchange. In our article ‘The best pillar 3a’, we compare different providers and show you what is important.

When is it worth starting?

It’s worth paying into your 3rd pillar as early as possible. This is particularly true if you are investing pillar 3a. This is because the long investment horizon allows you to take higher risks than you could with a short investment horizon. If you want to know more about when pillar 3a starts to pay off, you will find a more detailed answer in the linked article.

Should I choose active or passive funds?

Most providers offer you the choice between active or passive funds. Passive funds invest in an index and thus track a market. In contrast, the aim of active funds is to beat the market.

However, studies show that in the long term, the majority of actively managed funds do not outperform the market. What remains in the long term are the higher costs. For this reason, you are generally better off with passive 3a funds.

Which investment strategy is particularly suitable for pillar 3a?

Interest or dividends from pillar 3a pension funds are tax-free. An income-orientated strategy with a mix of shares, real estate and bonds therefore makes particular sense.

Investments such as gold or cryptocurrencies are less suitable. These investments do not generate current income, but are aimed at capital gains. The disadvantage: capital gains are tax-free in free assets, but not in pensions. They must be taxed upon withdrawal (keyword: capital withdrawal tax). It is therefore better not to invest pension assets in these asset classes.

What proportion of equities should I choose in pillar 3a?

The right investment strategy depends on your risk capacity. These three questions will help you make an assessment:

- How long is my investment horizon?

- How familiar am I with financial investments?

- Can I cope well with losses?

The longer you invest and the better you can deal with price fluctuations, the higher the proportion of equities you can invest in. If you are more security-orientated or need the money soon, you are better off with a defensive strategy or a 3a account.

Invest pillar 3a with finpension

With finpension, you can invest your pillar 3a in a targeted manner – simply, transparently and cost-effectively.

You can choose between six investment strategies with different proportions of equities. These strategies are each available in three variants: Global, Swiss and Sustainable. This allows you to find the solution that suits your risk profile and values. If you wish, you can also put together a completely customised strategy.

The annual management fee is a flat rate of 0.39 %. The investment strategies are generally implemented with fee-free funds (TER of 0.0%).